Machine Learning, Big Data Analytics, General AI, Specific AI, Digital Transformation, Natural Language Processing, Bots, Skills… there are a bewildering number of terms around the topic of Artificial Intelligence. The word seems to be a so-called „suitcase word“.

And indeed, the definitions are not yet clear and uniformly accepted. Term Artificial Intelligence in Germany is defined as „Information processing technology for independent solution of problems by computer“. This definition is very broad and quet different from a one used in US: „Artificial intelligence (AI) refers to the simulation of human intelligence in machines that are programmed to think like humans and mimic their actions. The term may also be applied to any machine that exhibits traits associated with a human mind such as learning and problem-solving“.

Independently from the definition or even the number of areas, which are subordered to the term, the importance and the future position of Artificial Intelligence is undisptutable. Considering the high number of investments and inflow of ventuire capital in USA, China and also rising volume of onflow in Germany the significance of such a disruptive technology for all areas of economy is not subject to discussion.

The below report is related to the innovation survey in 2019. Approximately 17,500 german companies, from several economical sectors, have been surveyed in the course of the study.

Official numbers

In November 2018, the German government’s artificial intelligence strategy was adopted. The Federal Government is thus setting a framework for a holistic political design of the further development and application of artificial intelligence in Germany. So it is obvious that artifical intelligence a key technology in the near future, also in Germany. The rapid, efficient and effective exploitation of application areas of AI is a decisive factor in maintaining the innovative strength and competitiveness of the German economy. The report below will display some central stat’s and numbers representing the position of Artificial Intelligence as a technology from the economical perspective.

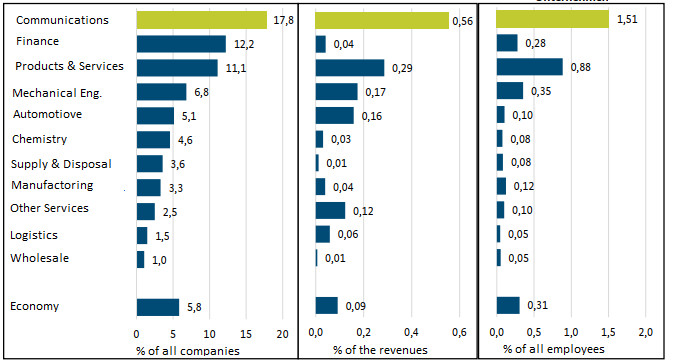

In 2019, around 17500 companies were active in the field of AI or were using this technology in their own companies. . The ranking below considering the ration of all companies as a total number. The second factor the ratio cionsideruing the revenues generated by the usage of Artificial Intelligence. The last factor representign the number of employees working at AI either as a key or a supportative ressource. It is not surprising that Communications and IT sector is leading in all 3 factors.

The expenses for research and development of AI were 4.8 billion dollars in Germany, which is only 2,7 % of the entire R&D budget. In US the overall invest into the AI as a technilogy has exceeded 16.9 billion dollars. The ratio between the R&D expenses and the future importance of AI is not really traceable. Especially because of the fact the significance of the technology is reported as crucial by more than a half of all companies – 65% see the AI as a unique point while competing in the own market.

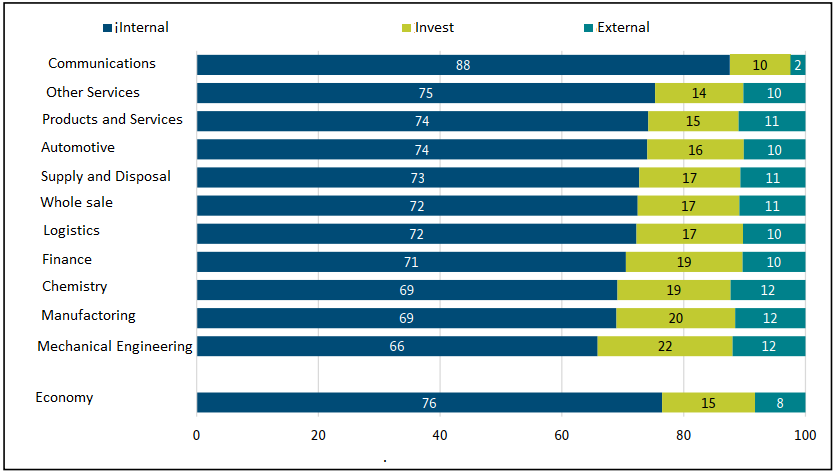

Considering the expenses for AI development it is important to mention that the almost 76% of those are related to the company – internal applications. The main part of those spendings are for the personell ressources. This is explainable by the fact the most software-building blocks are available as a open source. So the most time consuming activity is the development and application of available source to the internal needs.

The internal expenses are related to the human capital, development of internal application, hardware and IT peripherals. The external spendings are located to the commercial acquisition of the software or development sevices.

The total revenue from the AI products and servies in Germany amounts to 60 billions €. The main part of this income is provided by the financial services, around 17%. For a closer look of the revenue distribution among the producing companies a further distinction is needed. Thus it is required to split the producing companies in thise, which are concentrating their businesses explicitly on the AI, and those, where AI is not the centtral product or service. The companies with a specific AI-focus generated 7,7% of their entire revenue from the AI and releated products. Financial services is leading the ranking with the amount of 14% of the total revenue.

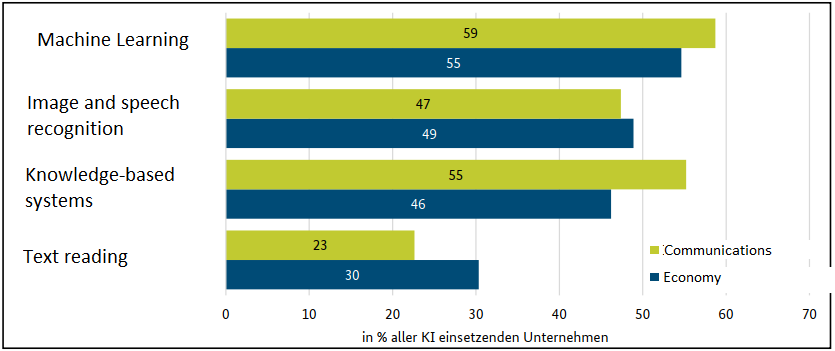

The most widely used technology in Germany is the machine learning. The second place is hold by the knowledge-based systems (e.g. AI-based methods for the identification, representation and processing of knowledge).

Mostly the AI as a technology is provided to the customers by the means of a product or service – around 60%. Another area of operation is the automation of the processes, which is taking arounf 56% of the Areas of application of AI processes in companies in the German economy. AI deployment spans different functional areas of enterprises. According to the AI is frequently used in products or services, the functional area of production and production/service provision leads the way in both the ICT sector (57%) and the economy as a whole (52%). (52%) at the top. On average, 37% of companies in the economy as a whole use AI in administration. administration. In the functional areas of R&D/innovation and information technology, around 20 % of companies use their AI applications. In the R&D/innovation area, it can be both the use of AI for R&D processes, but also activities to develop AI solutions. The use of AI in the areas of marketing/sales (5%) and purchasing/logistics (3%) is relatively low.

At the end

At the end the Artificial Intelligence in Germany is rising as a technological area, even though the inflow of venture and investmetn capital into R&D and respective start-up’s is very low compared to another main competitors (e.g. USA, China). This appears incomprehensible, especially in the Kontext of the future significance and state of Artificial Intelligence. Considering the current state of AI it is conspicuous that the most benefiting economical sector is the one of financial services. This is explainable by the fact this operational area is able to provide a huge amount of data, which is extremelly important for the learning algorithms. At this point it is important to mention that more than 70% of the data used by financial services during application of the AI is considered as a personal data.

On another hand it is dubious, why medical services and respective products are not even represented in the survey. This leads to the assumption that the development of AI in the medical field is very underdeveloped. Considering the importance of the predective medicine in the coming years this should be corrected. Due to the lack of human capital and experience most companies interested in application of AI to internal processes are in need to request the AI as a service or a product from external providers. For around 60% of all companies AI is developed and provided by an external provider. This reinforces the trend that AI_related products will be offered as a service – AIaaS.